Python Tutorial Part III--Clean OptionMetrics

April 7, 2017 | Michael Gong

1. Clean OptionMetrics dataset

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

%matplotlib inline

raw = pd.read_csv('5Firms.csv.zip',parse_dates=[2,3])

raw.drop(columns=['secid','issuer','exercise_style','last_date'],inplace=True)

raw.head(5)

|

date |

exdate |

cp_flag |

strike_price |

best_bid |

best_offer |

volume |

open_interest |

imvol |

delta |

optionid |

ticker |

index_flag |

midquo |

| 14 |

2012-01-03 |

2012-01-21 |

C |

34.000 |

9.300 |

10.250 |

0 |

0 |

0.529 |

0.988 |

70433772 |

COF |

0 |

9.775 |

| 15 |

2012-01-03 |

2012-01-21 |

C |

35.000 |

8.600 |

9.200 |

0 |

1237 |

0.666 |

0.948 |

45658102 |

COF |

0 |

8.900 |

| 16 |

2012-01-03 |

2012-01-21 |

C |

36.000 |

7.350 |

8.300 |

0 |

10 |

0.515 |

0.965 |

67966062 |

COF |

0 |

7.825 |

| 17 |

2012-01-03 |

2012-01-21 |

C |

37.000 |

6.800 |

7.050 |

0 |

4 |

0.550 |

0.929 |

70433773 |

COF |

0 |

6.925 |

| 18 |

2012-01-03 |

2012-01-21 |

C |

38.000 |

5.850 |

6.000 |

0 |

589 |

0.481 |

0.921 |

54279804 |

COF |

0 |

5.925 |

<class 'pandas.core.frame.DataFrame'>

Int64Index: 4467804 entries, 14 to 5719675

Data columns (total 14 columns):

date datetime64[ns]

exdate datetime64[ns]

cp_flag object

strike_price float64

best_bid float64

best_offer float64

volume int64

open_interest int64

imvol float64

delta float64

optionid int64

ticker object

index_flag int64

midquo float64

dtypes: datetime64[ns](2), float64(6), int64(4), object(2)

memory usage: 511.3+ MB

# change the implied volatility name (it's too long)

raw.rename(columns={'impl_volatility': 'imvol'}, inplace=True)

# transform the strike price and calculate the mid quotes

raw['strike_price'] = raw['strike_price'] / 1000.0

raw['midquo'] = (raw['best_bid'] + raw['best_offer']) / 2

raw.head(5)

|

date |

exdate |

cp_flag |

strike_price |

best_bid |

best_offer |

volume |

open_interest |

imvol |

delta |

optionid |

ticker |

index_flag |

midquo |

| 14 |

2012-01-03 |

2012-01-21 |

C |

0.034 |

9.300 |

10.250 |

0 |

0 |

0.529 |

0.988 |

70433772 |

COF |

0 |

9.775 |

| 15 |

2012-01-03 |

2012-01-21 |

C |

0.035 |

8.600 |

9.200 |

0 |

1237 |

0.666 |

0.948 |

45658102 |

COF |

0 |

8.900 |

| 16 |

2012-01-03 |

2012-01-21 |

C |

0.036 |

7.350 |

8.300 |

0 |

10 |

0.515 |

0.965 |

67966062 |

COF |

0 |

7.825 |

| 17 |

2012-01-03 |

2012-01-21 |

C |

0.037 |

6.800 |

7.050 |

0 |

4 |

0.550 |

0.929 |

70433773 |

COF |

0 |

6.925 |

| 18 |

2012-01-03 |

2012-01-21 |

C |

0.038 |

5.850 |

6.000 |

0 |

589 |

0.481 |

0.921 |

54279804 |

COF |

0 |

5.925 |

# drop contracts with NaN implied volatility or Nan delta

raw.dropna(subset=['imvol'], how='any', inplace=True)

raw.dropna(subset=['delta'], how='any', inplace=True)

# Exclude implied volatility above 150%

raw = raw[raw['imvol'] < 1.5]

# Exclude price below 0.05

raw = raw[raw['best_offer'] > 0.05]

raw.head(5)

|

date |

exdate |

cp_flag |

strike_price |

best_bid |

best_offer |

volume |

open_interest |

imvol |

delta |

optionid |

ticker |

index_flag |

midquo |

| 14 |

2012-01-03 |

2012-01-21 |

C |

0.034 |

9.300 |

10.250 |

0 |

0 |

0.529 |

0.988 |

70433772 |

COF |

0 |

9.775 |

| 15 |

2012-01-03 |

2012-01-21 |

C |

0.035 |

8.600 |

9.200 |

0 |

1237 |

0.666 |

0.948 |

45658102 |

COF |

0 |

8.900 |

| 16 |

2012-01-03 |

2012-01-21 |

C |

0.036 |

7.350 |

8.300 |

0 |

10 |

0.515 |

0.965 |

67966062 |

COF |

0 |

7.825 |

| 17 |

2012-01-03 |

2012-01-21 |

C |

0.037 |

6.800 |

7.050 |

0 |

4 |

0.550 |

0.929 |

70433773 |

COF |

0 |

6.925 |

| 18 |

2012-01-03 |

2012-01-21 |

C |

0.038 |

5.850 |

6.000 |

0 |

589 |

0.481 |

0.921 |

54279804 |

COF |

0 |

5.925 |

# calculate maturity

raw['maturity'] = ((raw['exdate'] - raw['date']) / np.timedelta64(1, 'D')).astype(int)

# Exclude contracts with maturity longer than 240 days and shorter than 7 days

raw = raw[(raw['maturity'] <= 360) & (raw['maturity'] >= 7)]

raw.head(5)

|

date |

exdate |

cp_flag |

strike_price |

best_bid |

best_offer |

volume |

open_interest |

imvol |

delta |

optionid |

ticker |

index_flag |

midquo |

maturity |

| 14 |

2012-01-03 |

2012-01-21 |

C |

0.034 |

9.300 |

10.250 |

0 |

0 |

0.529 |

0.988 |

70433772 |

COF |

0 |

9.775 |

18 |

| 15 |

2012-01-03 |

2012-01-21 |

C |

0.035 |

8.600 |

9.200 |

0 |

1237 |

0.666 |

0.948 |

45658102 |

COF |

0 |

8.900 |

18 |

| 16 |

2012-01-03 |

2012-01-21 |

C |

0.036 |

7.350 |

8.300 |

0 |

10 |

0.515 |

0.965 |

67966062 |

COF |

0 |

7.825 |

18 |

| 17 |

2012-01-03 |

2012-01-21 |

C |

0.037 |

6.800 |

7.050 |

0 |

4 |

0.550 |

0.929 |

70433773 |

COF |

0 |

6.925 |

18 |

| 18 |

2012-01-03 |

2012-01-21 |

C |

0.038 |

5.850 |

6.000 |

0 |

589 |

0.481 |

0.921 |

54279804 |

COF |

0 |

5.925 |

18 |

# save the cleaned raw data, because it is time-consuming to processing, next time we just need to load it

hdf = pd.HDFStore('hdf.h5')

hdf['raw'] = raw

hdf.close()

# if next time we start from here

# hdf = pd.HDFStore('hdf.h5')

# raw = hdf['raw']

# hdf.close()

2. Some summary statistics

# select variable we want

clean = raw[['date', 'ticker', 'imvol', 'delta', 'maturity', 'cp_flag']].reset_index(drop=True)

clean.head(5)

|

date |

ticker |

imvol |

delta |

maturity |

cp_flag |

| 0 |

2012-01-03 |

COF |

0.529 |

0.988 |

18 |

C |

| 1 |

2012-01-03 |

COF |

0.666 |

0.948 |

18 |

C |

| 2 |

2012-01-03 |

COF |

0.515 |

0.965 |

18 |

C |

| 3 |

2012-01-03 |

COF |

0.550 |

0.929 |

18 |

C |

| 4 |

2012-01-03 |

COF |

0.481 |

0.921 |

18 |

C |

print('stocks ticker:\n',clean['ticker'].unique())

print('maturity range:\n',clean['maturity'].min(),clean['maturity'].max())

print('delta range:\n',clean['delta'].min(),clean['delta'].max())

stocks ticker:

['COF' 'DD' 'XOM' 'INTC' 'SPX' 'UNH']

maturity range:

7 360

delta range:

-0.999934 0.999999

stats = clean.groupby(['ticker','cp_flag'])[['imvol','delta']].describe()

stats

|

|

imvol |

delta |

|

|

count |

mean |

std |

min |

25% |

50% |

75% |

max |

count |

mean |

std |

min |

25% |

50% |

75% |

max |

| ticker |

cp_flag |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| COF |

C |

100419.000 |

0.295 |

0.146 |

0.063 |

0.199 |

0.249 |

0.341 |

1.000 |

100419.000 |

0.523 |

0.359 |

0.008 |

0.130 |

0.577 |

0.884 |

1.000 |

| P |

108812.000 |

0.319 |

0.144 |

0.057 |

0.213 |

0.280 |

0.386 |

1.000 |

108812.000 |

-0.372 |

0.340 |

-1.000 |

-0.710 |

-0.240 |

-0.059 |

-0.003 |

| DD |

C |

125769.000 |

0.264 |

0.138 |

0.063 |

0.178 |

0.217 |

0.299 |

0.999 |

125769.000 |

0.553 |

0.366 |

0.008 |

0.146 |

0.639 |

0.917 |

1.000 |

| P |

134941.000 |

0.262 |

0.105 |

0.047 |

0.187 |

0.233 |

0.313 |

0.999 |

134941.000 |

-0.392 |

0.352 |

-1.000 |

-0.760 |

-0.255 |

-0.063 |

-0.004 |

| INTC |

C |

113863.000 |

0.306 |

0.150 |

0.084 |

0.218 |

0.248 |

0.331 |

1.000 |

113863.000 |

0.577 |

0.349 |

0.015 |

0.209 |

0.660 |

0.922 |

1.000 |

| P |

127602.000 |

0.293 |

0.113 |

0.074 |

0.221 |

0.260 |

0.334 |

1.000 |

127602.000 |

-0.505 |

0.359 |

-1.000 |

-0.882 |

-0.514 |

-0.122 |

-0.007 |

| SPX |

C |

1240711.000 |

0.245 |

0.151 |

0.050 |

0.139 |

0.202 |

0.297 |

1.000 |

1240711.000 |

0.674 |

0.361 |

0.001 |

0.373 |

0.869 |

0.970 |

1.000 |

| P |

1344534.000 |

0.259 |

0.135 |

0.033 |

0.157 |

0.233 |

0.326 |

1.000 |

1344534.000 |

-0.251 |

0.328 |

-1.000 |

-0.419 |

-0.066 |

-0.010 |

-0.000 |

| UNH |

C |

86588.000 |

0.280 |

0.133 |

0.076 |

0.204 |

0.236 |

0.303 |

1.000 |

86588.000 |

0.536 |

0.364 |

0.007 |

0.141 |

0.600 |

0.904 |

1.000 |

| P |

92393.000 |

0.290 |

0.118 |

0.066 |

0.213 |

0.255 |

0.333 |

0.999 |

92393.000 |

-0.395 |

0.352 |

-1.000 |

-0.759 |

-0.271 |

-0.058 |

-0.003 |

| XOM |

C |

112332.000 |

0.240 |

0.140 |

0.034 |

0.156 |

0.187 |

0.265 |

1.000 |

112332.000 |

0.535 |

0.358 |

0.006 |

0.148 |

0.601 |

0.889 |

1.000 |

| P |

126483.000 |

0.244 |

0.110 |

0.039 |

0.169 |

0.213 |

0.287 |

0.999 |

126483.000 |

-0.418 |

0.353 |

-1.000 |

-0.796 |

-0.316 |

-0.073 |

-0.003 |

# constant

clean['const'] = 1

# scaled moneyness

clean['delta_n'] = clean['delta']

clean.loc[(clean['cp_flag']=='P'),'delta_n'] = 1 + clean.loc[(clean['cp_flag']=='P'),'delta']

clean['delta_n'] = clean['delta_n'] - 0.5

# scaled maturity

clean['matur_n'] = clean['maturity']/360 - 0.5

# quadratic term of moneyness

clean['delta2'] = clean['delta_n']**2

# interaction between maturity and moneyness

clean['inter'] = clean['delta_n']*clean['matur_n']

clean.head(5)

|

date |

ticker |

imvol |

delta |

maturity |

cp_flag |

const |

delta_n |

matur_n |

delta2 |

inter |

| 0 |

2012-01-03 |

COF |

0.529 |

0.988 |

18 |

C |

1 |

0.488 |

-0.450 |

0.239 |

-0.220 |

| 1 |

2012-01-03 |

COF |

0.666 |

0.948 |

18 |

C |

1 |

0.448 |

-0.450 |

0.201 |

-0.202 |

| 2 |

2012-01-03 |

COF |

0.515 |

0.965 |

18 |

C |

1 |

0.465 |

-0.450 |

0.216 |

-0.209 |

| 3 |

2012-01-03 |

COF |

0.550 |

0.929 |

18 |

C |

1 |

0.429 |

-0.450 |

0.184 |

-0.193 |

| 4 |

2012-01-03 |

COF |

0.481 |

0.921 |

18 |

C |

1 |

0.421 |

-0.450 |

0.177 |

-0.189 |

4. Cross-section regression

import statsmodels.api as sm

4.1 straightforward way

tickers = clean['ticker'].unique()

ticker = tickers[0]

tmp = clean[clean['ticker']==ticker]

dates = tmp['date'].unique()

tmp = tmp[tmp['date']==dates[0]]

tmp.head(5)

|

date |

ticker |

imvol |

delta |

maturity |

cp_flag |

const |

delta_n |

matur_n |

delta2 |

inter |

| 0 |

2012-01-03 |

COF |

0.529 |

0.988 |

18 |

C |

1 |

0.488 |

-0.450 |

0.239 |

-0.220 |

| 1 |

2012-01-03 |

COF |

0.666 |

0.948 |

18 |

C |

1 |

0.448 |

-0.450 |

0.201 |

-0.202 |

| 2 |

2012-01-03 |

COF |

0.515 |

0.965 |

18 |

C |

1 |

0.465 |

-0.450 |

0.216 |

-0.209 |

| 3 |

2012-01-03 |

COF |

0.550 |

0.929 |

18 |

C |

1 |

0.429 |

-0.450 |

0.184 |

-0.193 |

| 4 |

2012-01-03 |

COF |

0.481 |

0.921 |

18 |

C |

1 |

0.421 |

-0.450 |

0.177 |

-0.189 |

exogs = ['const','delta_n','matur_n','delta2','inter']

mB = np.linalg.lstsq(tmp[exogs],tmp['imvol'])[0]

array([ 0.272, 0.176, -0.170, 0.920, 0.054])

4.2 More concise way

def CrossReg(df,exogs):

mod = sm.OLS(df['imvol'],df[exogs]).fit()

ind = pd.MultiIndex.from_product([['params','tvalues'],exogs])

ret = pd.Series(index=ind)

ret.loc['params'] = mod.params.values

ret.loc['tvalues'] = mod.tvalues.values

ret.loc['r2'] = mod.rsquared

return ret

exogs = ['const','delta_n','matur_n','delta2','inter']

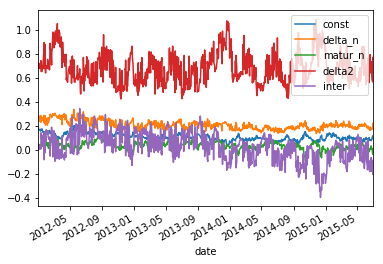

mB = clean.groupby(['ticker','date']).apply(lambda x:CrossReg(x,exogs))

mB.loc['SPX']['params'].plot()

<matplotlib.axes._subplots.AxesSubplot at 0x7f2d109103c8>

4.3 Need for speed

4.3.1 Just for coefficients, sequential

def CrossRegSpeed(df,exogs):

mB = np.linalg.lstsq(df[exogs],df['imvol'])[0]

return pd.Series(mB,index=exogs)

mB = clean.groupby(['ticker','date']).apply(lambda x:CrossRegSpeed(x,exogs))

4.3.2 Just for coefficients, parallel

import multiprocessing as mp

from functools import partial

def CrossRegParHelper(ticker):

tmp = DATA[DATA['ticker']==ticker]

mB = tmp.groupby(['date']).apply(lambda x:CrossRegSpeed(x,EXOGS))

mB['ticker'] = ticker

return mB

def CrossRegPar(data,exogs):

global DATA, EXOGS

DATA = data

EXOGS = exogs

pool = mp.Pool(processes=12)

results = pool.map(CrossRegParHelper, tickers)

pool.close()

pool.join()

mB = pd.concat(results)

return mB

mB = CrossRegPar(clean,exogs)

%timeit clean.groupby(['ticker','date']).apply(lambda x:CrossRegSpeed(x,exogs))

8 s ± 33.4 ms per loop (mean ± std. dev. of 7 runs, 1 loop each)

%timeit CrossRegPar(clean,exogs)

4.2 s ± 51.4 ms per loop (mean ± std. dev. of 7 runs, 1 loop each)

4.3.3 JIT compilation

clean.sort_values(by=['ticker','date'],inplace=True)

locs = clean.groupby(['ticker','date']).size().values.cumsum()

locs = np.insert(locs,0,0)

mY = clean[['imvol']].values

mX = clean[exogs].values

@nb.jit

def CrossRegJIT(mX,mY,locs):

N = locs.shape[0]

mB = np.zeros((mX.shape[1],N-1))

for i in range(0,N-1):

b = np.linalg.lstsq(mX[locs[i]:locs[i+1]],mY[locs[i]:locs[i+1]])[0]

mB[:,[i]] = b

return mB

mB = CrossRegJIT(mX,mY,locs)

%timeit CrossRegJIT(mX,mY,locs)

702 ms ± 6.65 ms per loop (mean ± std. dev. of 7 runs, 1 loop each)

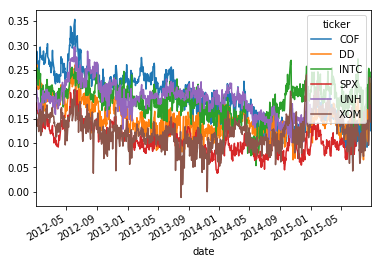

mB = pd.DataFrame(mB.T,index=clean.groupby(['ticker','date']).size().index,columns=exogs)

|

const |

delta_n |

matur_n |

delta2 |

inter |

ticker |

| date |

|

|

|

|

|

|

| 2012-01-03 |

0.272 |

0.176 |

-0.170 |

0.920 |

0.054 |

COF |

| 2012-01-04 |

0.288 |

0.079 |

-0.090 |

1.023 |

-0.263 |

COF |

| 2012-01-05 |

0.288 |

0.160 |

-0.129 |

0.776 |

-0.110 |

COF |

| 2012-01-06 |

0.251 |

0.246 |

-0.149 |

1.189 |

0.076 |

COF |

| 2012-01-09 |

0.267 |

0.176 |

-0.167 |

0.881 |

0.312 |

COF |

5. Principal Component Analysis

mB.reset_index(inplace=True)

level = pd.pivot_table(mB,index='date',columns='ticker',values='const')

from sklearn import preprocessing

import scipy as sp

def pcaAnalysis(mX, iPC, useCov=1):

if useCov:

# mCov = np.cov(mX, rowvar = 0)

de_meanX = mX - np.tile(np.mean(mX, axis=0), [mX.shape[0], 1])

mCov = np.dot(de_meanX.transpose(), de_meanX) / mX.shape[0]

eigval, eigvec = sp.linalg.eigh(mCov)

eigidx = np.argsort(eigval)

maxidx = eigidx[::-1]

sorted_vec = eigvec[:, maxidx]

mPC = np.dot(de_meanX, sorted_vec)

return mPC[:, 0:iPC], (eigval[maxidx] / np.sum(eigval))[0:iPC]

else:

mCoef = np.corrcoef(mX, rowvar=0)

scaled_X = preprocessing.scale(mX)

eigval, eigvec = sp.linalg.eigh(mCoef)

eigidx = np.argsort(eigval)

maxidx = eigidx[::-1]

sorted_vec = eigvec[:, maxidx]

mPC = np.dot(scaled_X, sorted_vec)

return preprocessing.scale(mPC[:, 0:iPC]), (eigval[maxidx] /

np.sum(eigval))[0:iPC]

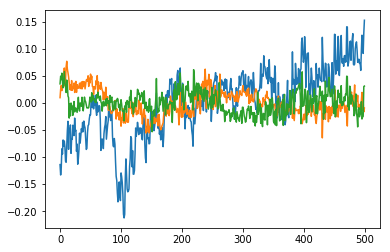

mPC,pct = pcaAnalysis(level.values[:500],3)

pct

array([ 7.22e-01, 9.53e-02, 6.82e-02])

[<matplotlib.lines.Line2D at 0x7f054028cb70>,

<matplotlib.lines.Line2D at 0x7f054028c518>,

<matplotlib.lines.Line2D at 0x7f054028cf28>]