Python Tutorial Part II--Numpy and Pandas

April 3, 2017 | Michael Gong1. Numpy/Scipy

NumPy and SciPy are open-source add-on modules to Python that provide common mathematical and numerical routines in pre-compiled, fast functions. These are growing into highly mature packages that provide functionality that meets, or perhaps exceeds, that associated with common commercial software like MatLab.

The NumPy (Numeric Python) package provides basic routines for manipulating large arrays and matrices of numeric data.

The SciPy (Scientific Python) package extends the functionality of NumPy with a substantial collection of useful algorithms, like minimization, Fourier transformation, regression, and other applied mathematical techniques.

import numpy as np Matlab to Numpy translation click here

Numpy Complete documentation click here

Scipy Complete documentation click here

print(np.__version__)

np.__config__.show()1.11.2

openblas_lapack_info:

NOT AVAILABLE

blas_mkl_info:

libraries = ['mkl_intel_lp64', 'mkl_intel_thread', 'mkl_core', 'iomp5', 'pthread']

include_dirs = ['/home/michael/anaconda3/include']

define_macros = [('SCIPY_MKL_H', None), ('HAVE_CBLAS', None)]

library_dirs = ['/home/michael/anaconda3/lib']

lapack_mkl_info:

libraries = ['mkl_intel_lp64', 'mkl_intel_thread', 'mkl_core', 'iomp5', 'pthread']

include_dirs = ['/home/michael/anaconda3/include']

define_macros = [('SCIPY_MKL_H', None), ('HAVE_CBLAS', None)]

library_dirs = ['/home/michael/anaconda3/lib']

blas_opt_info:

libraries = ['mkl_intel_lp64', 'mkl_intel_thread', 'mkl_core', 'iomp5', 'pthread']

include_dirs = ['/home/michael/anaconda3/include']

define_macros = [('SCIPY_MKL_H', None), ('HAVE_CBLAS', None)]

library_dirs = ['/home/michael/anaconda3/lib']

lapack_opt_info:

libraries = ['mkl_intel_lp64', 'mkl_intel_thread', 'mkl_core', 'iomp5', 'pthread']

include_dirs = ['/home/michael/anaconda3/include']

define_macros = [('SCIPY_MKL_H', None), ('HAVE_CBLAS', None)]

library_dirs = ['/home/michael/anaconda3/lib']1.1 Array creation

a = np.array([1,2,3])

print(type(a))

print(a)<class 'numpy.ndarray'>

[1 2 3]b = np.array([[1,2,3],[3,4,5]])

print("this is b\n",b)

print("the shape of b is:",b.shape)

print("the dimension of b is:",b.ndim)

print("number of elements of b:", b.size)this is b

[[1 2 3]

[3 4 5]]

the shape of b is: (2, 3)

the dimension of b is: 2

number of elements of b: 6** A little bit introduction of object oriented programming**

a = np.array([1,2,3,3,4,5,5,6,7])

print("the type of a:",type(a))

b = a.reshape(3,3)

print("the type of b:",type(b))

c1 = b**2

print("the type of c:",type(c1))

# we can write:

c2 = np.array([1,2,3,3,4,5,5,6,7]).reshape(3,3)**2

print(np.allclose(c1,c2))the type of a: <class 'numpy.ndarray'>

the type of b: <class 'numpy.ndarray'>

the type of c: <class 'numpy.ndarray'>

True1.2 Array operation

# generate random ndarray

mA = np.random.randint(1,10,size=(3,3))

mB = np.random.randint(1,10,size=(3,3))

vC = np.random.randint(1,10,size=(3,1))

vD = np.random.randint(1,10,size=(1,3))

print("mA:\n",mA)

print("mB:\n",mB)

print("vC:\n",vC)

print("vD:\n",vD)mA:

[[8 9 6]

[1 3 7]

[5 3 2]]

mB:

[[6 7 1]

[3 2 4]

[5 8 2]]

vC:

[[9]

[1]

[2]]

vD:

[[3 6 8]]element-wise operation *,/,+,-

print(mA+mB)[[14 16 7]

[ 4 5 11]

[10 11 4]]print(mA-mB)[[ 2 2 5]

[-2 1 3]

[ 0 -5 0]]print(mA/mB)[[ 1.33333333 1.28571429 6. ]

[ 0.33333333 1.5 1.75 ]

[ 1. 0.375 1. ]]print(mA*mB)[[48 63 6]

[ 3 6 28]

[25 24 4]]print(mA-vC)[[-1 0 -3]

[ 0 2 6]

[ 3 1 0]]print(mA-vD)[[ 5 3 -2]

[-2 -3 -1]

[ 2 -3 -6]]print(mA*mB-vC + mB**2)[[ 75 103 -2]

[ 11 9 43]

[ 48 86 6]]Matrix operation

Matrix mupliplication @

# The matrix multiplication is done by @ operation (in python 3.0+), in python 2.*, it is done by "dot" method

print(mA@mB)[[105 122 56]

[ 50 69 27]

[ 49 57 21]]Matrix transpose T

print(mA.T)[[8 1 5]

[9 3 3]

[6 7 2]]Matrix inversion “inv”

print(np.linalg.inv(mA))

# to make it easier to type, we import the "inv" function alone

from numpy.linalg import inv

print(inv(mA))[[ -1.42857143e-01 6.93889390e-18 4.28571429e-01]

[ 3.14285714e-01 -1.33333333e-01 -4.76190476e-01]

[ -1.14285714e-01 2.00000000e-01 1.42857143e-01]]

[[ -1.42857143e-01 6.93889390e-18 4.28571429e-01]

[ 3.14285714e-01 -1.33333333e-01 -4.76190476e-01]

[ -1.14285714e-01 2.00000000e-01 1.42857143e-01]]# again, we can benefit from the OOP design

ret = mA.T@inv(mB) - vC + mB.T@vC - vD

print(ret)[[ 57.5 53.89285714 47.46428571]

[ 80. 75.28571429 69.42857143]

[ 12.75 9.23214286 7.16071429]]1.3 Slicing

A = np.random.rand(3,3)

print(A)

print(A[:,[0]])[[ 0.07731399 0.10377817 0.1793915 ]

[ 0.84609483 0.65710391 0.17246314]

[ 0.7439164 0.89687702 0.1211748 ]]

[[ 0.07731399]

[ 0.84609483]

[ 0.7439164 ]]# slicing is done through bracket []

print(mA)

print('the first element is:\n',mA[0,0])

print('the first column is:\n',mA[:,[0]])

print('the first two columns are:\n',mA[:,:2])

# boolean and integer indexing

indexB = np.array([True, False, True])

indexI = np.array([1,0,1])

array = np.array([1,2,3])

print("Boolean indexing result:\n" ,array[indexB])

print("Integer indexing result:\n", array[indexI])[[8 9 6]

[1 3 7]

[5 3 2]]

the first element is:

8

the first column is:

[[8]

[1]

[5]]

the first two columns are:

[[8 9]

[1 3]

[5 3]]

Boolean indexing result:

[1 3]

Integer indexing result:

[2 1 2]1.4 Frequently used Numpy function

- diag: create diagonal matrix from vector

- diagonal: extract the diagonal element

- eye: identity matrix

- zeros: matrix filled with zero

- ones: matrix filled with one

- reshape: reshape the matrix

vY = np.random.rand(3)

print(vY.shape,type(vY))(3,) <class 'numpy.ndarray'>print(np.diag(vY))[[ 0.36944492 0. 0. ]

[ 0. 0.46322172 0. ]

[ 0. 0. 0.80256682]]print(np.diagonal(np.diag(vY)))[ 0.36944492 0.46322172 0.80256682]print(np.eye(3))[[ 1. 0. 0.]

[ 0. 1. 0.]

[ 0. 0. 1.]]print(np.zeros([3,3]))

print(np.ones([3,3]))[[ 0. 0. 0.]

[ 0. 0. 0.]

[ 0. 0. 0.]]

[[ 1. 1. 1.]

[ 1. 1. 1.]

[ 1. 1. 1.]]print(np.zeros_like(vY))

print(np.zeros_like(np.diag(vY)))[ 0. 0. 0.]

[[ 0. 0. 0.]

[ 0. 0. 0.]

[ 0. 0. 0.]]# benefits of the OOS design

print((np.diag(vY)+np.random.rand(3,3)).reshape(9,1).max()**2)1.386368103441.5 Some example and exercises

(1) Subtract the mean of each row of a matrix

a = np.random.rand(3,3)

b = a - a.mean(axis=1) #np.mean(a,axis=1)

print(b)[[-0.27371758 -0.13738752 0.631215 ]

[-0.25698583 -0.11128908 0.68699173]

[-0.30855162 0.03770426 -0.26797938]](2) compute the moving average of an array

def moving_average(vY,window):

T = vY.shape[0]

ret = np.zeros(T - window)

for j,t in enumerate(range(window,T)):

ret[j] = vY[t-window:t].mean()

return ret

vY = np.random.rand(20)

window = 5

ret = moving_average(vY,window)

print(ret)[ 0.31439101 0.3067207 0.2612112 0.4488305 0.51791912 0.40021872

0.5155174 0.60879213 0.60470478 0.58250843 0.57880459 0.60341439

0.62814638 0.6328429 0.73670997](3) find the closest point

def find_closePointV1(points,target):

min_distance = 1

point_index = 0

for i,point in enumerate(points):

distance = ((point-target)**2).sum()

if distance < min_distance:

min_distance = distance

point_index = i

return min_distance,point_index

def find_closePointV2(points,target):

distances = ((points-target)**2).sum(axis=1)

min_distance = distances.min()

point_index = distances.argmin()

return min_distance,point_indexpoints = np.random.rand(2000,2)

target = np.array([0.5,0.5])

min_distance1,point_index1 = find_closePointV1(points,target)

min_distance2,point_index2 = find_closePointV2(points,target)

print("Version 1 the minimum distance:",min_distance1)

print("Version 1 the point with minimum distance",points[point_index1])

print("Version 2 the minimum distance:",min_distance2)

print("Version 2 the point with minimum distance",points[point_index2])Version 1 the minimum distance: 0.000113540004683

Version 1 the point with minimum distance [ 0.50663792 0.50833535]

Version 2 the minimum distance: 0.000113540004683

Version 2 the point with minimum distance [ 0.50663792 0.50833535]# version 1 and version 2 have huge performance difference

%timeit find_closePointV1(points,target)100 loops, best of 3: 5.76 ms per loop%timeit find_closePointV2(points,target)The slowest run took 4.57 times longer than the fastest. This could mean that an intermediate result is being cached.

10000 loops, best of 3: 46.9 µs per loop(4) One line code of simulation of Pi

N = 1000000

pi = 4*((np.random.rand(N,2)**2).sum(axis=1)<1).sum()/N

print(pi)3.1411642. Pandas

Pandas is an open source, BSD-licensed library providing high-performance, easy-to-use data structures and data analysis tools for the Python programming language.

- Use Pandas as possible as you can!

import pandas as pd2.1 ** Object creation**

index = [i for i in range(4)]

columns = ['A','B','C','D','E']

data = pd.DataFrame(np.random.rand(4,5),index=index,columns=columns)

print(data) A B C D E

0 0.377511 0.935913 0.484039 0.494305 0.017102

1 0.674354 0.961497 0.719836 0.463993 0.966345

2 0.113718 0.558731 0.725746 0.287497 0.447674

3 0.799740 0.051104 0.585415 0.475480 0.6512202.2 ** Selction**

data['A']0 0.582853

1 0.205175

2 0.142668

3 0.517169

Name: A, dtype: float64data[['A','B']]| A | B | |

|---|---|---|

| 0 | 0.582853 | 0.050482 |

| 1 | 0.205175 | 0.676394 |

| 2 | 0.142668 | 0.728272 |

| 3 | 0.517169 | 0.224242 |

data[0:3]| A | B | C | D | E | |

|---|---|---|---|---|---|

| 0 | 0.582853 | 0.050482 | 0.257578 | 0.340971 | 0.907032 |

| 1 | 0.205175 | 0.676394 | 0.830756 | 0.963753 | 0.675394 |

| 2 | 0.142668 | 0.728272 | 0.353043 | 0.082804 | 0.585398 |

# Label based selection

data.loc[3,'B']0.22424205926919127data.loc[0:2,['A','B']]| A | B | |

|---|---|---|

| 0 | 0.582853 | 0.050482 |

| 1 | 0.205175 | 0.676394 |

| 2 | 0.142668 | 0.728272 |

# integer based selection

data.iloc[1:4,0:2]| A | B | |

|---|---|---|

| 1 | 0.205175 | 0.676394 |

| 2 | 0.142668 | 0.728272 |

| 3 | 0.517169 | 0.224242 |

data.iloc[1:3,:]| A | B | C | D | E | |

|---|---|---|---|---|---|

| 1 | 0.205175 | 0.676394 | 0.830756 | 0.963753 | 0.675394 |

| 2 | 0.142668 | 0.728272 | 0.353043 | 0.082804 | 0.585398 |

data.ix[1:3]| A | B | C | D | E | |

|---|---|---|---|---|---|

| 1 | 0.205175 | 0.676394 | 0.830756 | 0.963753 | 0.675394 |

| 2 | 0.142668 | 0.728272 | 0.353043 | 0.082804 | 0.585398 |

| 3 | 0.517169 | 0.224242 | 0.585978 | 0.654013 | 0.965902 |

# Boolean indexing

indexB = data['A'] > 0.2

print(indexB)

print(data[indexB])0 True

1 True

2 False

3 True

Name: A, dtype: bool

A B C D E

0 0.582853 0.050482 0.257578 0.340971 0.907032

1 0.205175 0.676394 0.830756 0.963753 0.675394

3 0.517169 0.224242 0.585978 0.654013 0.965902# or conveniently

print(data[data['A']>0.2]) A B C D E

0 0.582853 0.050482 0.257578 0.340971 0.907032

1 0.205175 0.676394 0.830756 0.963753 0.675394

3 0.517169 0.224242 0.585978 0.654013 0.965902# OOP

data[data['A']>0.2]['C'].ix[0]0.257577504604104222.3 Arithmatic operations

data['F'] = (data['A'] + data['B'])/data['C'] - data['D']*data['E']

print(data) A B C D E F

0 0.772780 0.251506 0.638696 0.712863 0.639697 1.147697

1 0.723921 0.383294 0.007697 0.661608 0.638037 143.427074

2 0.808509 0.679512 0.296928 0.872748 0.898736 4.227009

3 0.226408 0.768940 0.292466 0.896504 0.974840 2.5293432.4 Apply

def func(series):

return series.sum()/series.std()

ret = data.apply(func,axis=1)

data['ret'] = data.apply(func,axis=1)

print(ret)

print('\n')

print(data)0 5.779099

1 2.757361

2 6.135847

3 5.855379

dtype: float64

A B C D E F ret

0 0.772780 0.251506 0.638696 0.712863 0.639697 1.147697 5.779099

1 0.723921 0.383294 0.007697 0.661608 0.638037 143.427074 2.757361

2 0.808509 0.679512 0.296928 0.872748 0.898736 4.227009 6.135847

3 0.226408 0.768940 0.292466 0.896504 0.974840 2.529343 5.8553792.5 Groupby

This is a extremely useful object, please go through the detail cookbook

By “group by” we are referring to a process involving one or more of the following steps

- Splitting the data into groups based on some criteria

- Applying a function to each group independently

- Combining the results into a data structure

data = pd.DataFrame({'A' : ['foo', 'bar', 'foo', 'bar',

'foo', 'bar', 'foo', 'foo'],

'B' : ['one', 'one', 'two', 'three',

'two', 'two', 'one', 'three'],

'C' : np.random.randn(8),

'D' : np.random.randn(8)})

data| A | B | C | D | |

|---|---|---|---|---|

| 0 | foo | one | 0.785 | -0.553 |

| 1 | bar | one | 0.724 | 1.079 |

| 2 | foo | two | -1.760 | -0.818 |

| 3 | bar | three | 0.721 | 0.440 |

| 4 | foo | two | 0.026 | 0.068 |

| 5 | bar | two | 0.442 | 0.321 |

| 6 | foo | one | -0.328 | 0.176 |

| 7 | foo | three | -0.473 | -1.483 |

groupA = data.groupby('A')

groupAB = data.groupby(['A','B'])

print(groupA)

print(groupAB)<pandas.core.groupby.generic.DataFrameGroupBy object at 0x7eff7ff467b8>

<pandas.core.groupby.generic.DataFrameGroupBy object at 0x7eff7ff46128># GroupBy object attributes

groupA.groups{'bar': Int64Index([1, 3, 5], dtype='int64'),

'foo': Int64Index([0, 2, 4, 6, 7], dtype='int64')}# some statistics

# Std

print(groupAB.std())

# Mean

print(groupAB.mean())

# Sum

print(groupAB.sum()) C D

A B

bar one NaN NaN

three NaN NaN

two NaN NaN

foo one 0.287689 0.533024

three NaN NaN

two 0.259739 0.182370

C D

A B

bar one 0.093289 -1.435398

three 1.610691 0.099456

two 1.674365 -1.969331

foo one -0.433944 0.118717

three 0.640498 0.695818

two 1.002847 -0.708532

C D

A B

bar one 0.093289 -1.435398

three 1.610691 0.099456

two 1.674365 -1.969331

foo one -0.867888 0.237433

three 0.640498 0.695818

two 2.005694 -1.417063Iteration through groups

for group_name, group_data in groupA:

print('group name: ',group_name)

print('group data:\n',group_data)

print('\n')group name: bar

group data:

A B C D

1 bar one -1.763415 -1.015387

3 bar three -1.104977 -2.578075

5 bar two -1.650251 -0.601321

group name: foo

group data:

A B C D

0 foo one 0.738800 0.320824

2 foo two -0.866414 -0.223506

4 foo two 0.009047 -0.798006

6 foo one 0.209088 -0.120664

7 foo three -0.470803 0.823928# you can flexibly run function on group data, for example: OLS regression

beta = np.zeros(2)

for i, (group_name,group_data) in enumerate(groupA):

mY = group_data[['C']].values

mX = group_data[['D']].values

beta[i] = np.linalg.lstsq(mX,mY)[0]

print(beta)[ 0.7005281 0.00695643]# the method above is very flexible, you can use another useful method: group apply

def myfunc(group_data):

print(group_data)

mY = group_data[['C']].values

mX = group_data[['D']].values

return np.linalg.lstsq(mX,mY)[0]

groupA.apply(myfunc) B C D

1 one -1.763415 -1.015387

3 three -1.104977 -2.578075

5 two -1.650251 -0.601321

B C D

1 one -1.763415 -1.015387

3 three -1.104977 -2.578075

5 two -1.650251 -0.601321

B C D

0 one 0.738800 0.320824

2 two -0.866414 -0.223506

4 two 0.009047 -0.798006

6 one 0.209088 -0.120664

7 three -0.470803 0.823928

A

bar [[0.700528102717]]

foo [[0.00695642969842]]

dtype: objectdef myfunc(group_data):

mY = group_data[['C']].values

mX = group_data[['D']].values

return float(np.linalg.lstsq(mX,mY)[0])

result = groupA.apply(myfunc)

print(result)A

bar 0.700528

foo 0.006956

dtype: float64def myfunc(group_data):

# if the return result is a dataframe, pandas will look at its index, and merge the result back to original

# dataframe by same index

return (group_data['C']/group_data['D'].sum()).to_frame('ret')

data['ret'] = data.groupby('A').apply(myfunc)

data| A | B | C | D | ret | |

|---|---|---|---|---|---|

| 0 | foo | one | -0.230517 | -0.258188 | 0.476460 |

| 1 | bar | one | 0.093289 | -1.435398 | -0.028224 |

| 2 | foo | two | 1.186510 | -0.579577 | -2.452417 |

| 3 | bar | three | 1.610691 | 0.099456 | -0.487309 |

| 4 | foo | two | 0.819184 | -0.837487 | -1.693185 |

| 5 | bar | two | 1.674365 | -1.969331 | -0.506574 |

| 6 | foo | one | -0.637371 | 0.495621 | 1.317392 |

| 7 | foo | three | 0.640498 | 0.695818 | -1.323855 |

2.6 Merge data

This is another power object, please go through detail

basic syntax:

pd.merge(left, right, how='inner', on=None, left_on=None, right_on=None,

left_index=False, right_index=False, sort=True,

suffixes=('_x', '_y'), copy=True, indicator=False)left = pd.DataFrame({'key': ['K0', 'K1', 'K2', 'K3'],

'A': ['A0', 'A1', 'A2', 'A3'],

'B': ['B0', 'B1', 'B2', 'B3']})

right = pd.DataFrame({'key': ['K1', 'K2', 'K3', 'K4'],

'C': ['C0', 'C1', 'C2', 'C3'],

'D': ['D0', 'D1', 'D2', 'D3']})

print(left)

print(right) A B key

0 A0 B0 K0

1 A1 B1 K1

2 A2 B2 K2

3 A3 B3 K3

C D key

0 C0 D0 K1

1 C1 D1 K2

2 C2 D2 K3

3 C3 D3 K4inner_merged = pd.merge(left,right,how='inner',left_on=['key'],right_on=['key'])

print(inner_merged) A B key C D

0 A1 B1 K1 C0 D0

1 A2 B2 K2 C1 D1

2 A3 B3 K3 C2 D2left_merged = pd.merge(left,right,how='left',left_on=['key'],right_on=['key'])

print(left_merged) A B key C D

0 A0 B0 K0 NaN NaN

1 A1 B1 K1 C0 D0

2 A2 B2 K2 C1 D1

3 A3 B3 K3 C2 D22.7 Pivot and reshape table

…Again…very power object, details click here

data = pd.DataFrame({'A' : ['foo', 'bar', 'foo', 'bar',

'foo', 'bar', 'foo', 'foo'],

'B' : ['one', 'one', 'two', 'three',

'two', 'two', 'one', 'three'],

'C' : np.random.randn(8),

'D' : np.random.randn(8)})

data| A | B | C | D | |

|---|---|---|---|---|

| 0 | foo | one | 1.329326 | 0.515690 |

| 1 | bar | one | 0.912863 | -0.309627 |

| 2 | foo | two | -0.219018 | 2.094762 |

| 3 | bar | three | -0.159688 | 0.737186 |

| 4 | foo | two | 1.182747 | 0.359100 |

| 5 | bar | two | -0.013464 | -1.514432 |

| 6 | foo | one | -1.277657 | 0.657462 |

| 7 | foo | three | 0.012385 | 0.535246 |

table = pd.pivot_table(data,index=['A'],columns=['B'],values=['C'])

print(table) C

B one three two

A

bar 0.912863 -0.159688 -0.013464

foo 0.025835 0.012385 0.4818652.7 Useful funciton on DataFrame

data.describe()data.describe(percentiles=[0.2,0.3,0.4,0.8])# shape

data.shape# transpose

data.T# link to numpy

data_values = data.values

print(type(data_values))

print(data_values)# caveat, data_values is a "VIEW" of the DataFrame, which means that it is mutable!

data_values[0,0] = 15

data3. Learn Pandas by example

import matplotlib.pyplot as plt

%matplotlib inline

data = pd.read_csv('data.csv')

data.head(6)| Date | minor | Open | High | Low | Close | Volume | Adj Close | |

|---|---|---|---|---|---|---|---|---|

| 0 | 2010-01-04 | AAPL | 213.430 | 214.500 | 212.380 | 214.010 | 123432400.000 | 27.727 |

| 1 | 2010-01-04 | INTC | 20.790 | 21.030 | 20.730 | 20.880 | 47800900.000 | 16.443 |

| 2 | 2010-01-04 | MSFT | 30.620 | 31.100 | 30.590 | 30.950 | 38409100.000 | 25.555 |

| 3 | 2010-01-05 | AAPL | 214.600 | 215.590 | 213.250 | 214.380 | 150476200.000 | 27.775 |

| 4 | 2010-01-05 | INTC | 20.940 | 20.990 | 20.600 | 20.870 | 52357700.000 | 16.435 |

| 5 | 2010-01-05 | MSFT | 30.850 | 31.100 | 30.640 | 30.960 | 49749600.000 | 25.564 |

data.info()<class 'pandas.core.frame.DataFrame'>

RangeIndex: 5412 entries, 0 to 5411

Data columns (total 8 columns):

Date 5412 non-null object

minor 5412 non-null object

Open 5412 non-null float64

High 5412 non-null float64

Low 5412 non-null float64

Close 5412 non-null float64

Volume 5412 non-null float64

Adj Close 5412 non-null float64

dtypes: float64(6), object(2)

memory usage: 338.3+ KB# change the column name

data.rename(columns={'minor':'ticker'},inplace=True)

data.head(5)| Date | ticker | Open | High | Low | Close | Volume | Adj Close | |

|---|---|---|---|---|---|---|---|---|

| 0 | 2010-01-04 | AAPL | 213.430 | 214.500 | 212.380 | 214.010 | 123432400.000 | 27.727 |

| 1 | 2010-01-04 | INTC | 20.790 | 21.030 | 20.730 | 20.880 | 47800900.000 | 16.443 |

| 2 | 2010-01-04 | MSFT | 30.620 | 31.100 | 30.590 | 30.950 | 38409100.000 | 25.555 |

| 3 | 2010-01-05 | AAPL | 214.600 | 215.590 | 213.250 | 214.380 | 150476200.000 | 27.775 |

| 4 | 2010-01-05 | INTC | 20.940 | 20.990 | 20.600 | 20.870 | 52357700.000 | 16.435 |

data.sort_values(by=['ticker','Date'],inplace=True)

data.head(5)| Date | ticker | Open | High | Low | Close | Volume | Adj Close | |

|---|---|---|---|---|---|---|---|---|

| 0 | 2010-01-04 | AAPL | 213.430 | 214.500 | 212.380 | 214.010 | 123432400.000 | 27.727 |

| 3 | 2010-01-05 | AAPL | 214.600 | 215.590 | 213.250 | 214.380 | 150476200.000 | 27.775 |

| 6 | 2010-01-06 | AAPL | 214.380 | 215.230 | 210.750 | 210.970 | 138040000.000 | 27.333 |

| 9 | 2010-01-07 | AAPL | 211.750 | 212.000 | 209.050 | 210.580 | 119282800.000 | 27.283 |

| 12 | 2010-01-08 | AAPL | 210.300 | 212.000 | 209.060 | 211.980 | 111902700.000 | 27.464 |

data['Date'] = pd.to_datetime(data['Date'].astype(str), format='%Y-%m-%d')

data.info()<class 'pandas.core.frame.DataFrame'>

Int64Index: 5412 entries, 0 to 5411

Data columns (total 8 columns):

Date 5412 non-null datetime64[ns]

ticker 5412 non-null object

Open 5412 non-null float64

High 5412 non-null float64

Low 5412 non-null float64

Close 5412 non-null float64

Volume 5412 non-null float64

Adj Close 5412 non-null float64

dtypes: datetime64[ns](1), float64(6), object(1)

memory usage: 380.5+ KB# if we only interested in adjusted close price, we can pivot the table

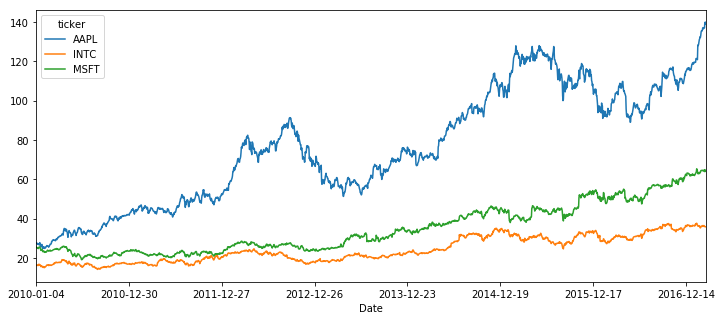

close_price = pd.pivot_table(data,index='Date',columns='ticker',values='Adj Close')close_price.head(6)| ticker | AAPL | INTC | MSFT |

|---|---|---|---|

| Date | |||

| 2010-01-04 | 27.727 | 16.443 | 25.555 |

| 2010-01-05 | 27.775 | 16.435 | 25.564 |

| 2010-01-06 | 27.333 | 16.380 | 25.407 |

| 2010-01-07 | 27.283 | 16.222 | 25.143 |

| 2010-01-08 | 27.464 | 16.403 | 25.316 |

| 2010-01-11 | 27.222 | 16.498 | 24.994 |

close_price.plot(figsize=(12,5))<matplotlib.axes._subplots.AxesSubplot at 0x7eff568117b8>

# if we want the return, Pandas provide an extremely easy transformation

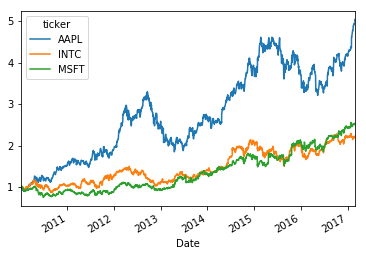

stock_return = close_price.pct_change()

stock_return.head(5)| ticker | AAPL | INTC | MSFT |

|---|---|---|---|

| Date | |||

| 2010-01-04 | NaN | NaN | NaN |

| 2010-01-05 | 0.001729 | -0.000479 | 0.000323 |

| 2010-01-06 | -0.015906 | -0.003354 | -0.006137 |

| 2010-01-07 | -0.001849 | -0.009615 | -0.010400 |

| 2010-01-08 | 0.006648 | 0.011165 | 0.006897 |

#plot the cumulative return in one line

(1+stock_return).cumprod().plot()<matplotlib.axes._subplots.AxesSubplot at 0x7f76333135f8>

# just show the style of OOP

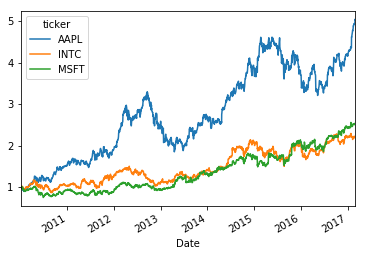

(1 + pd.pivot_table(data,index='Date',columns='ticker',values='Adj Close').pct_change()).cumprod().plot()

# save the return dataframe to csv

stock_return.to_csv('stockReturn.csv')# or, to save it to HDF5 format, which is much faster

# create a HDF store

hdf = pd.HDFStore('stock.h5')

hdf['stock_return'] = stock_return

hdf['raw_data'] = data

hdf.close()%timeit data = pd.read_csv('data.csv')100 loops, best of 3: 5.75 ms per loophdf = pd.HDFStore('stock.h5')

%timeit data = hdf['raw_data']The slowest run took 6.86 times longer than the fastest. This could mean that an intermediate result is being cached.

100 loops, best of 3: 2.61 ms per loop